Ijraset Journal For Research in Applied Science and Engineering Technology

Arima Model with Box-Cox Transformed Univariate Variable in BSE Sensex

Authors: N Ramachandra, M Bhupathi Naidu, Sk Nafeez Umar, K Murali

DOI Link: https://doi.org/10.22214/ijraset.2022.47509

Certificate: View Certificate

Abstract

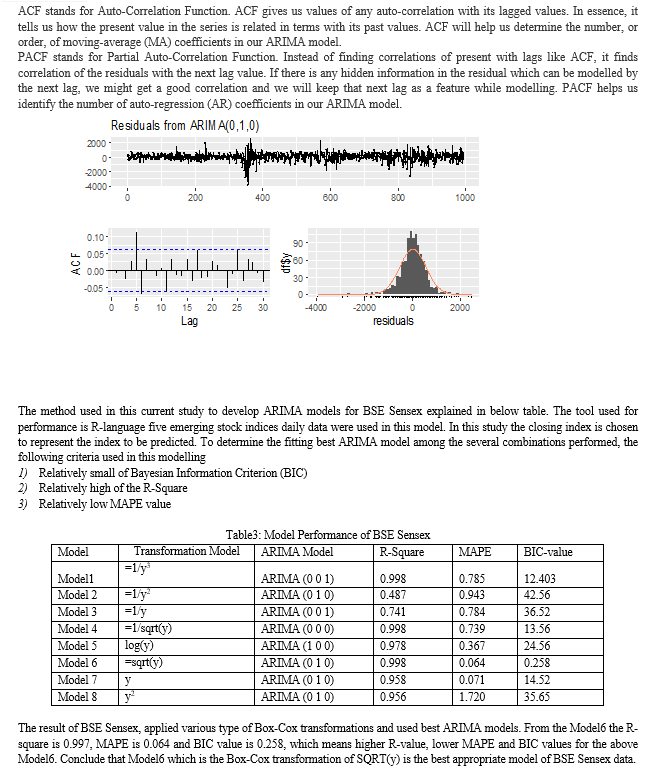

Fluctuation of the stock market’s impact on investments of stocks. Sensex prediction plays an important role in the investment of markets. Predicting the stock market is difficult in market scenarios. The present study attempted to predict the stock market due to its complicated features and also compared different Auto-Regressive Integrated Moving Average (ARIMA) models to get the appropriate stock forecasting model using various Box-Cox transformations by using BSE Sensex past daily closing data. The ARIMA Model6 (0 1 0) showed accurate results in calculating the Mean Absolute Percentage Error (MAPE) and Bayesian Information Criterion (BIC) values, which indicates the potential of using the ARIMA model for accurate stock forecasting.

Introduction

I. INTRODUCTION

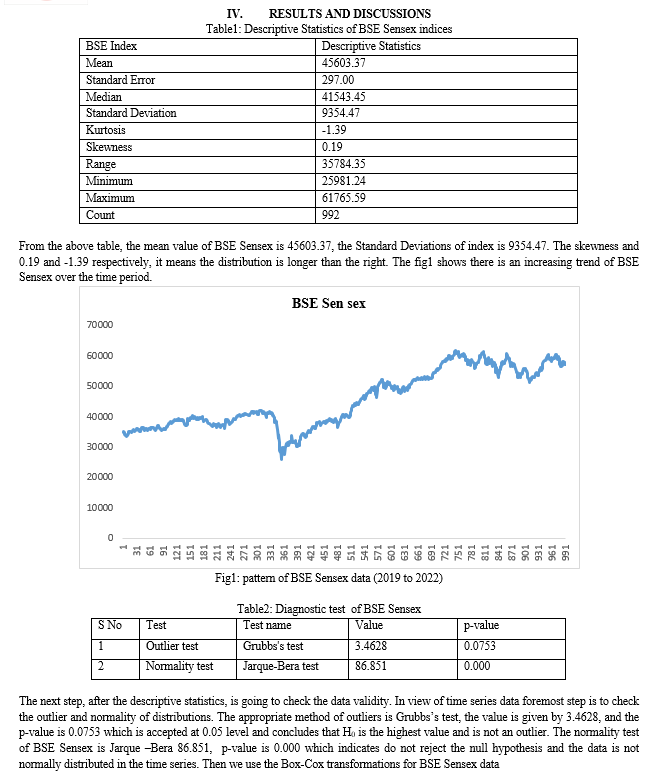

Closing prices or returns on stock prices or closing values of the market as a whole is a kind of time series which in the series analysis is classified under “general random walk”. This is a non-stationary time series which means its mean or other statistical properties change over time. The present study is the forecasting of the BSE Sensex index of stock and the daily BSE Sensex index data series. This is daily data series of the BSE Sensex index.

The following is the description of the data set used in the research study.

As per the review collected from various articles, many researchers have investigated volatility time series modeling of the different stock markets, mainly focusing on U.S and Indian stock markets. Some of the researchers have focused on the Indian stock market with ARIMA Model. The foremost drive of the study is to deepen the knowledge about stock market volatility in National Stock Exchange.

Rakesh Gupta (2012) aimed to forecast the volatility of stock markets belonging to the five founder members of the Association of South-East Asian Nations, referred to as the ASEAN-5 by using Asymmetric-PARCH (APARCH) models with two different distributions (Student-t and GED). The result showed that APARCH models with t-distribution usually perform better.

Praveen (2011) investigated BSE SENSEX, BSE 100, BSE 200, BSE 500, CNX NIFTY, CNX 100, CNX 200 and CNX 500 by employing ARCH/GARCH time series models to examine the volatility in the Indian financial market during 2000-14. The study concluded that extreme volatility during the crisis period has affected the volatility in the Indian financial market for a long duration.

Philip Hans Franses & Dick Van Dijk (1996) Forecasting stock market volatility using (nonlinear) GARCH model, as per the finding of the study Q GARCH model is best when the estimation sample does not content extreme observations such as the 1987 stock market crash and the GJR model cannot be recommended for forecasting. In their estimation of volatility they used Within Sample Estimation and Out of Sample estimation and found that the forecasting performance of the GARCH type models appears sensitive to extreme within-sample observations.

Srinivasan et al. (2010) attempted to forecast the volatility (conditional variance) of the SENSEX Index returns using daily data, covering a period from 1st January 1996 to 29th January 2010. The result showed that the symmetric GARCH model do perform better in forecasting conditional variance of the SENSEX Index return rather than the asymmetric GARCH models

Floros (2008) the researcher has investigated the volatility using daily data from two Middle East stock indices viz., the Egyptian CMA index and the Israeli tase-100 index, and has used various models, GARCH, EGARCH, TGARCH, Component GARCH (CGARCH), and Power GARCH (PGARCH).

The study found that the coefficient of the EGARCH model showed a negative and significant value for both indices, indicating the existence of the leverage effect. AGARCH model showed weak transitory leverage effects in the conditional variances and the study showed that increased risk would not necessarily lead to an increase in returns.

II. MATERIAL AND METHODS

The Bombay Stock Exchange (BSE) data were considered for applying the time series models like ARIMA using various Box-Cox transformations in the time series data. The present study is based on the daily closing market index for the Bombay Stock Exchange (BSE). Actively performing BSE Sensex (Aug 2008-Aug 2022) used for forecasting modes. In this study, Statistical software and R- language were used for the forecasting model building.

III. DIAGNOSTIC CHECKING

A. Outliers Checking

An outlier is a value or an observation that is distant from another observation, differs point that differs significantly from other data points Grubbs's test is based on the assumption of normality to check whether the data follows normality or not. This is the foremost step for data should have any outliers.

That is, one should first verify that the data can be reasonably approximated by a normal distribution before applying the Grubbs test.

Grubbs's test detects one outlier at a time. Grubbs's test is defined for the hypothesis:

H0: There are no outliers in the data set, Ha: There is exactly one outlier in the data set

The Grubbs test statistic is defined as

Conclusion

Difficult to the building of forecasting models mostly in time series data. Mainly in stock market data very oscillates over time. Forecasting with Auto ARIMA models provides a prediction based on historical data, in which data has been tested stationary and employed first-order differences to remove white noise problems. In this study, Auto ARIMA estimated BIC, MAPE, and R-Square which yielded a more accurate forecast over the time period and performance of the models. Thus, the study shows that the ARIMA model outperforms in forecasting BSE Sensex indices in terms of forecasting accuracy and in generating upcoming indexes.

References

[1] Philip (1996). “Forecasting stock market volatility using non- linear Garch models”, Journal of Forecasting, Vol. 15, pp. 229-235 [2] Floros Christos (2008). “Modelling volatility using GARCH models: Evidence from Egypt and Israel”, Middle Eastern Finance and Economics, No. 2, pp. 31-41 [3] Srinivasan P. and Ibrahim P. (2010). “Forecasting stock market volatility of Bse-30 index using Garch models”, pp. 47-60, available online at: https://journals.sagepub.com/doi/10.1177/097324701000600304 [4] Rakesh Gupta (2012). “Forecasting volatility of the ASEAN-5 stock markets: A nonlinear approach with non-normal errors”, Griffith University [5] Praveen Kulshreshtha (2011). “Volatility in the Indian financial market before, during and after the global financial crisis”, Journal of Accounting and Finance, Vol. 15, No. 3. [6] Shaik Nafeez Umar Shaik and, Labeeb Mohammed Zeeshan (2009), Journal of Business and Economics, ISSN 2155-7950, USA November 2019, Volume 10, No. 11, pp. 1045-1056 [7] Sk Nafeez Umar.,etl (2017) Forecasting Of Cotton Area, Production, Productivity Using Arima Models In Andhra Pradesh, Bulletin of Environment, Pharmacology and Life Sciences Bull. Env. Pharmacol. Life Sci., Vol 6 Special issue [3] 2017: 138-141

Copyright

Copyright © 2022 N Ramachandra, M Bhupathi Naidu, Sk Nafeez Umar, K Murali. This is an open access article distributed under the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original work is properly cited.

Download Paper

Paper Id : IJRASET47509

Publish Date : 2022-11-17

ISSN : 2321-9653

Publisher Name : IJRASET

DOI Link : Click Here

Submit Paper Online

Submit Paper Online