Ijraset Journal For Research in Applied Science and Engineering Technology

Economic Value Added: Acritical Reading

Authors: Dr. Ibrahim R. I. Elmadhoun, Mohammed H. K. Murtaja

DOI Link: https://doi.org/10.22214/ijraset.2022.40450

Certificate: View Certificate

Abstract

It is clear how important is the measure of Economic ?Value-Added? and preference that this measure has over traditional performance measures. This ?measure is based on creating value for the company, and this measure is distinguished by taking ?into account invested capital, whether owned or borrowed. In addition, studies have shown that ?the measure of Economic Value Added? increases the performance of the company and the ?performance of the management working. This measure affects the market value of the company ?and its use leads to maximizing the wealth of shareholders, and like all performance measures he ?has supporters and has critics. One of the criticisms directed against him is that he measures ?performance on the short level, as he cares about results, not causes, and the most important ?criticism directed at him is his dependence on accounting profit in the financial statements ?whether these statements represent the actual performance of the company or not.?

Introduction

I. INTRODUCTION

Modern management, in light of the development and progress in the field of technology, communications, and competition at the local and international levels tends to achieve shareholder value rather than profit interest only.

Despite the importance and utility of financial reports, there are deficiencies in these reports in meeting the needs of internal and external parties used for financial statements; therefore, financial analysts, investors, and economists have tended to develop these results and the trend towards calculating economic profit and not accounting profit because of its importance in the statement of economic value to the company. Therefore, maximizing the wealth of owners is considered the main goal of all business companies regardless of the nature of the business and type of company by stimulating the value of the company and directing all activities towards achieving this goal, while the value may take several forms which can be divided in two main ways: economic and non-economic. Many economists and researchers have developed measures to measure the actual performance and economic profit of companies. The extremely important measure is Economic Value-Added Measurement (EVA), developed by Stern & Stewart and published its concept as a brand under the name (EVA) and applied to large companies such as Coca-Cola company.

The measure of Economic Value Added has gained great fame as a measure that pays attention to economic profit and the creation of value for companies, and investors and managers have paid great attention to this measure, and many studies have shown the advantage of this measure). Research carried by (Senior Vice President of Stern Stewart & Co.), he underlined that of all the performance measuring methodologies employed by organizations. Nothing is more accurate than Economic Value Added, as firms that utilize it as a foundation for financial management have outperformed their competitors in a big manner. (Al Ehrbar, 1998).

Senior Vice President of Stern Stewart & Co. underlined that of all the measuring tools employed by organizations to gauge their success, the most important was Consumer satisfaction. Because organizations that utilize Economic Value Added as a framework for financial management have thrived in ways that are beneficial to their competition, there is no more accurate measure than Economic Value Added. (Al Ehrbar, 1998)

Because of the importance of Economic Value Added, this section will discuss in this topic the theoretical framework for it, the importance of the scale, the advantages and criticisms that were directed to this standard, and how it is calculated.

II. THE CONCEPT OF ECONOMIC VALUE ADDED

The concept of economic value as a thought goes back to Hamilton 1777 who wrote the book Introduction to Sales and Marshall 1890 who presented the book Principles of Economics in which he indicated that the returns of a business should exceed the cost of the capital owned and borrowed to increase Wealth: Marshall invented the concept of economic profit, on which Economic Value Added is built. Attention is attributed to the Economic Value Added to the American company Stewart & Stern, which was founded by (Joel Stern and Bennett Stewart) and which is concerned with financial management services and performance evaluation, as it provided the Economic Value Added as a measure of the company's economic performance, which according to the vision of Stewart & Stern is the best measurement. For performance compared to traditional accounting standards, which may be misleading about the actual performance of the company.

This "Economic Value Added" was defined by Stewart and Stern as the difference between adjusted net operating profit after taxes and the cost of owned and borrowed capital "as a measure of financial accomplishment tied to maximizing shareholder wealth over time" (Jiambalvo, 2007). It was defined by an earlier study (Ramana, 2005) as "the economic book value of capital at the beginning of the year plus the difference between the returns of capital and its cost"

Another study added (Irala, 2007) that the added economic value is a "tool that provides the investor with the returns of the monetary unit in a certain period through the profits of the invested capital after excluding its cost"

(Amarvathi and Raja, 2014) has defined it as "the amount of shareholder value added by management"

Siwasi added a definition of "the margin that results in the difference between the economic return generated by the institution for a specific period and the cost of the financial resources it used" (Siwasi, 2010)

He defined it (Al Bohairim, 2012) "It is the surplus value generated from the investment or the investment portfolio, equal to the additional return, the difference between the Return on Investment and the cost of the money used to finance this investment multiplied by the invested capital" As for (Scott, 2001), he defined it as the difference between what the owners of capital invested in the unit, and what they receive from the sale at the current prices prevailing in the stock market.

Through the above definitions, that all tariffs agreed that the Economic Value-Added add economic value to the company which is based on economic profit account and not the wind accounting and represents the value resulting from the investment and the financial cost of resources used in investment. In addition, the comprehensive definition of Economic Value Added that it is a measure of the value of measuring the extent of the added value on shareholder wealth through the operational processes in the organization as it is a measure of evaluating the performance of the managers of companies and represents the difference between the net operating profit after taxes and the cost of capital used in the process investment.

The Economic Value-Added scale is one of the most important performance measures for companies in recent decades. Below, the importance of the scale, the benefits, and criticisms directed at this scale will be clarified in addition to how it is calculated.

III. THE IMPORTANCE OF ECONOMIC VALUE ADDED

The Economic Value-Added measure is gaining in importance by creating an economic value for the company, the company is evaluated based on performance, not just accounting profit. Drucker (1995) has spoken that the company is still making losses unless its revenues cover the cost of the invested capital, regardless of whether it pays taxes as if it had made real profits.

The significance of the scale of added economic values lies in:

A. It Is the Correct Way to Calculate Shareholders' Profits (Returns)

The most important defining feature is the ability to enter the cost of capital into EVA accounts. Some businesses may look successful using standard accounting procedures, but many of them have not.

As a result, the primary premise is that the Economic Value Added is not used to determine whether or not a project or transaction is profitable. But how can you know if the profit generated is enough to cover the project's initial investment or was it used in another alternative opportunity? This can find a winning project from the point of view of accounting reports, while it is losing from the viewpoint of economic reports.

B. A Financial Standard That Executives Understand

Economic Value Added is characterized by its principles that are simple and easy to explain to managers in general and financial managers in particular, often non-financial managers find it difficult to understand some financial tools. Such as the concept of residual income or the concept of the future degree of growth and other traditional financial accounting terms and concepts. From here, the Economic Value Added can facilitate the process of communicating with them through easy understanding and also by raising the degree of solidarity and cooperation within the organization between the various managers.

C. Achieved Consistency Between Management Decisions and Shareholder Wealth

Economic Value Added is a concept created by Stern & Stewart to assist managers in making decisions based on two key financial bases:

- The First Rule: The primary financial goal of any company must be to increase shareholder wealth, which is in line with the modern managerial financial theory that works based on a basic premise. That the main purpose of the firm is to increase shareholder wealth.

- The Second Rule: The value of the firm depends on the degree to which investors expect the extent of future profits to exceed the cost of capital, where investors in the stock market are interested in the accounting profits published in the lists

Corporate finance when making their investment decisions, and when rebuilding their expectations and evaluating their investments will be affected in general by showing information about future profits, and then their effect on the company's stock price in the stock market in particular.

D. Remove Jamming and Multiple Targets.

To communicate financial goals, most businesses utilize a variety of criteria. Strategic plans, for example, are measured in terms of profits and market share, whereas goods and production lines within a plant are measured in terms of profit margins or cash flows.

While the business units are evaluated by return on capital, or by comparison to the level of profit expected in the budget. The inevitable result of inconsistencies in measurements, goals, and concepts often has negative repercussions for planning processes, strategies, and decisions. Whereas, the use of Economic Value Added avoids such confusion by using a single financial standard that links all types of decisions and makes them focused on one thing: how can shareholder wealth be increased.

(Stewart.1994) adds that Economic Value Added is the best measure of wealth creation today.

It is 50% higher than well-known accounting standards (Earning per share EPS, Return on Equity (ROE). This is explaining the changes in shareholders’ wealth.

Also some points explaining the importance of this measure:

- Shows the continuous and real improvement of the shareholders' wealth.

- It works as a basis for evaluating an effective incentive system and thus changing the behavior of individuals within the company.

- Increases managers' urges and encouragement to founders to work, as it contains a system of incentives for workers.

- It is allowed to evaluate financial decisions at their real value, as it is an important tool in making investment decisions.

IV. ADVANTAGES OF ECONOMIC VALUE ADDED (EVA)

The researchers' efforts recently moved to focus on finding the link between economics on the one hand and professional accounting practices on the other hand, and this interest came after the increasing frequency of criticisms directed at accounting data because of what it may involve errors or intentional or unintended misrepresentation, therefore, many companies have tended to use the Economic Value-Added measure, as many studies have demonstrated the preference of this measure, including (Stewart, 1991,1994,1999), (Sheehan, 1994), (Tully, 1993), (Grant, 2003), ( Stern, 2003) (Walbert, 1994) (Stern, Stewart and Chew, 1995), which is characterized by:

- When calculating profits according to the measure of Economic Value-Added, the cost of the capital owned and borrowed is taken into consideration, that is, all costs incurred by the institution are allocated from the realized revenues and therefore the realized profit represents the real profit of the shareholders.

- (Stern and Stewart) have proven, through their research, that the units applying the EVA measure performed better than their competitors by approximately (8-9) points annually about the total realized return of shareholders in the first five years from the start of this standard.

- The use of Economic Value Added by corporate management to make decisions would affect the assessment of the company's financial market, by directing judgment on internal financial performance through its effect on the values of its shares traded in the market, as the study demonstrated (Ferguson et al, 2005).

- The use of value-added information gives a good measure of the size and importance of the unit and its arrangement, which is better than using the sales number as a basis for ordering its importance and the size of the unit that may distort the truth because the sales number may be inflated with the costs of goods and services purchased from others and which are directly borne by consumers (Erasmus, 2008: Chen and Doddm 1997: Kim, 2006).

- The economic value achieved is directly related to the shareholders' wealth and draws the attention of the Corporation’s management to a performance that leads to an increase in the return to the shareholders.

- It works to reduce agency problems by motivating managers and encouraging them to act as owners of the company, as demonstrated by a study (Costigan and lovata, 2002: Biddle et al, 1999).

- A study (Lefkowitz, 1999: Peterson and Peterson, 1996: O’Byrne, 1996) demonstrated that the EVA scale has a strong correlation with the market value of the company as it is a measure to maximize the share price in the market.

V. THE STEPS FOR CALCULATING ECONOMIC VALUE ADDED

The “Economic Value Added” scale is used to determine the real profitability achieved by the company in order to achieve the “best value for shareholders”, so the method of calculating the Economic Value Added consists of five steps, as follows:

- Viewing and examining the financial statements of the units in the company: where the data that is approved is credited in calculating the added economic value that can be obtained from the financial statements.

- Determining the unit capital: The accounting principles that are acceptable in general are very often misleading in description The real financial situation of the unit indicated the cash capital that the unit invests, (Roztocki, Needy) has differentiated between the investment and operational capital where the operating capital is defined on the basis that it is the invested capital and minus the goodwill, cash and surplus stock from operating need.

- Adoption of the unit capital cost rate: One of the operations that depend on the Economic Value Added (EVA) per unit is the cost of capital, in small units, estimating the cost of capital is perhaps the most difficult part in calculating the Economic Value Added, and the cost of capital depends on the financial structure of the unit, business risks, level of current interest and investor expectations.

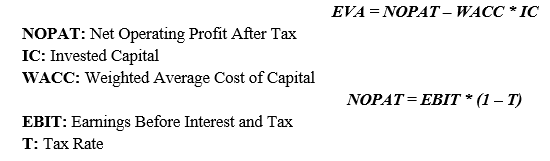

- Calculating the net operating profit of the unit after tax (NOPAT): The net operating profit of the unit measures the cash generation capacity of the unit from repeated business activities regardless of the capital structure.

- Calculation of the added economic value (EVA):

Economic Value Added (EVA) = net profit from operations after tax ± adjustments to operating profit - (weighted average cost of invested capital X (invested capital ± adjustments to budget elements))

The Economic Value Added is the difference between the net operating profit after taxes (NOPAT) and the cost of capital and is calculated according to the following formula (Stewart, 1991):

VI. SIMILARITIES AND DIFFERENCES BETWEEN THE ECONOMIC VALUE ADDED (EVA) MEASURE AND OTHER PERFORMANCE MEASURES

In light of the existence of a lot of performance measures, the spread of the concept of added economic value led to the emergence of what calls the perforation between measures and the abundance of talk about the best and most objective of these standards in measuring and evaluating the real performance of contemporary installations.

Accordingly, this part of the study discusses the similarities, differences, between EVA and some other measures, as the following scale:

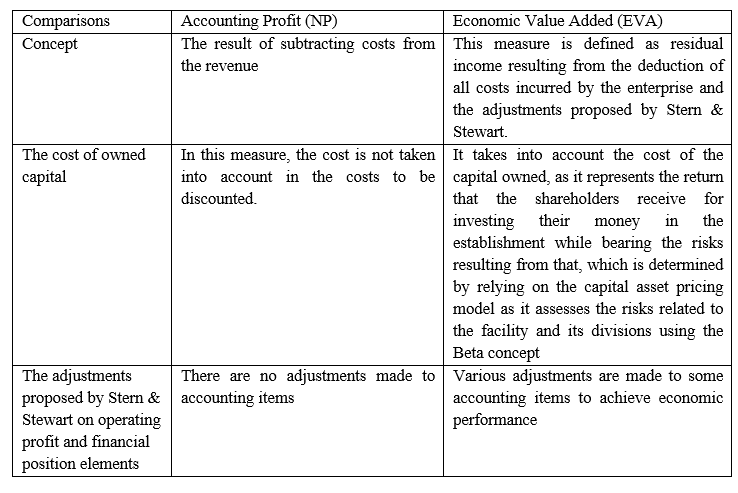

A. Economic Value Added (EVA) Measure and Accounting Profit - Net Profit (NP) Measure

Despite the dependence of the Economic Value Added (EVA) measure on the accounting profit as they are two measures that are relied upon in evaluating the performance of the facility management, they differ together in some points, including:

Accordingly, it is clear that the measure of accounting profit differs from the measure of economic value in the concept and goal that each seeks to reach.

Although both measures can be defined as residual income, this income varies due to the difference in the method of calculating it. When calculating the accounting profit NP, the costs are subtracted from the sales revenue, but this cost does not include the cost of the capital that is taken into account when calculating EVA, in addition, the profit measure is not intended to emphasize maximizing the value of shareholders, on the contrary, some decisions that increase these profits result in wasting the value of shareholders.

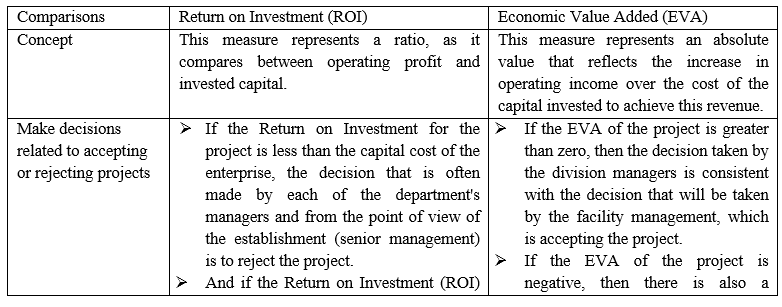

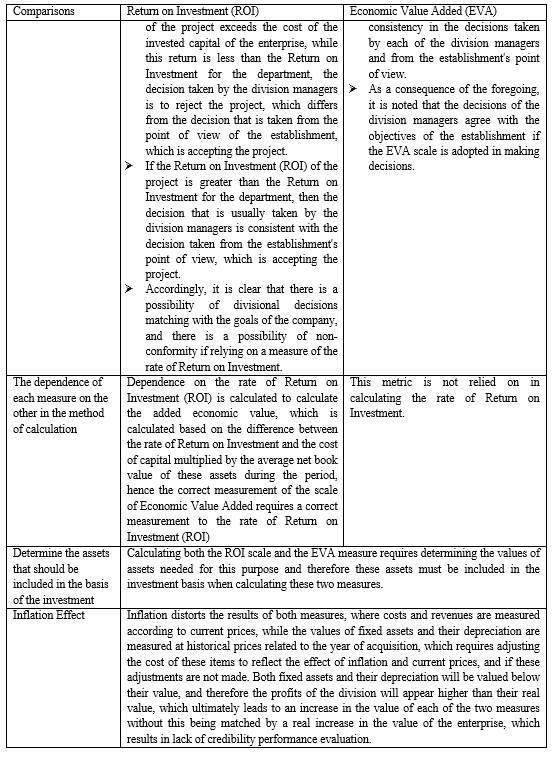

B. The Return on Investment (ROI) Rate Measure and The Economic Value Added (EVA) Measure

The comparison between the measure of Economic Value-Added and the rate of Return on Investment is based on the set of elements shown in the following table:

It can be concluded from the previous comparison between these two measures that they differ in the concept and goal and the decision to accept or reject projects. About the concept, the EVA scale expresses the increase in operating income over the cost of the invested capital, while the measure of the rate of Return on Investment divides the profit operating on invested capital.

Regarding the objective, the high value of the ROI does not mean achieving value for shareholders. With regard to the decision to accept or reject projects, in light of the EVA measure, there is a consistency between the department’s goals and the establishment’s goals, but this is not always achieved through relying on the measure of the rate of Return on Investment (ROI).

Despite the previous differences, however, each of the two measures requires that his account show the assets that must be covered by the basis of investment in addition to their agreement that inflation leads to distorting the results of each of them.

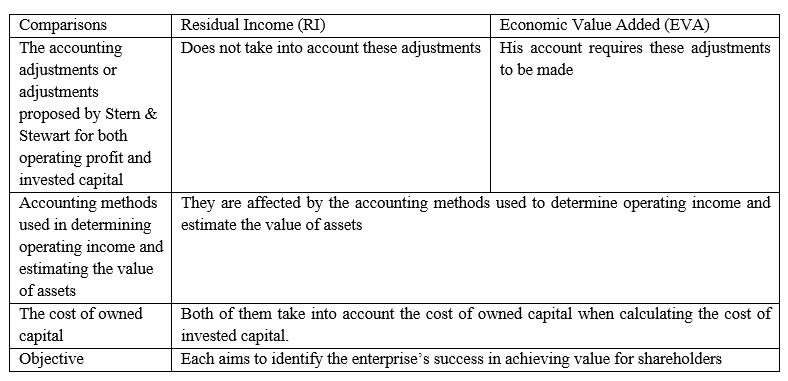

C. The Residual Income (RI) Measure and The Economic Value Added (EVA) Measure

The EVA measure is an extension of the Residual Income (RI) measure that appeared in the middle of the last century, and the following is a comparison between them through the following table:

From the above, it is clear that the EVA measure is consistent with the RI residual income scale in the concept. The first measure is an extension of the second. However, the EVA calculation requires a set of adjustments and adjustments proposed by Stern & Stewart on both operating profits and capital the money invested. With regards to this goal, each of them aims to ensure that the value for shareholders is achieved.

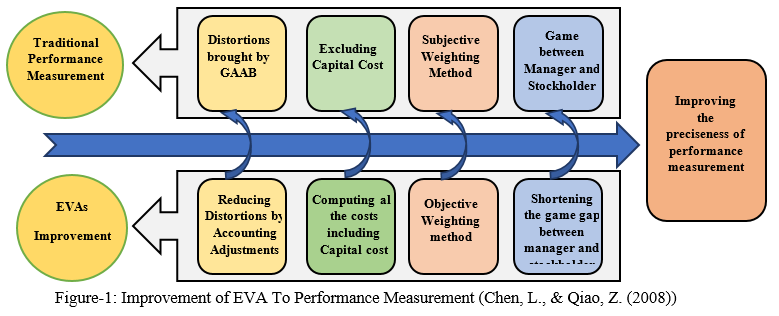

VII. CRITICISMS OF THE ECONOMIC VALUE ADDED

Despite the preference for the Economic Value-Added measure, and its ability to be better than other measures to give a true picture of profits and wealth growth for shareholders. There are some studies and researchers that have criticized this measure and among the most important of these studies (Biddle, Bowen, and Wallanc 1997: Chen and Dodd, 1997: 2001: Turvey et al., 2000: Lovat and Costigan, 2002: Peterson and Peterson, 1996). These studies found several deficiencies in the measure, as follows:

- Economic Value-Added evaluates short-term profitability and hence requires additional metrics to support it such as the degree of flexibility in manufacturing processes. The effectiveness of operations and production, the speed with which Consumer s' needs are met, and the level of employee satisfaction.

- The measure of Economic Value Added does not take into account differences in size. The reason for the decrease in the Economic Value Added of a particular department or unit in the company may be due to the difference in the volume of investment available to it.

- The calculation of the Economic Value Added depends on the value shown in the historical financial statements (after making the necessary adjustments) and therefore it reflects historical events and does not express value expectations in the future.

- Access to the Economic Value Added requires making any necessary adjustments to the net accounting income from operations. Some of these adjustments may be subject to personal estimates or may be adapted to harmonize with specific goals. There is no doubt that this will reduce their credibility and weaken their effectiveness.

- This measure is concerned with the results and not concerned with the causes and therefore it provides information that benefits only one aspect of performance which is the financial side and does not reflect the non-financial aspects of performance.

- The basis of Economic Value-Added depends on accounting profit, and accounting profit is weak with economic profit, as there is a conflict between accounting profit and economic profit in the event of increased inflation.

In addition, there are many studies that have shown the impact of Earnings Management through Real Earnings Management and Earnings Management through discretionary accruals. These studies are as follows:

Elmadhoun and Reddy (2022) This study found the negative effect of real earnings management on economic value added, the study targeted 52 companies from the Dubai Financial Market. In addition, Liu and Wang (2017) According to the findings of the research, there is a statistically significant positive relationship between profit management utilizing DA items and EVA in African countries. A substantial negative association between Earnings Management via DA items or REM activities and EVA has been found in G20 countries, and this relationship is statistically significant. Also Liu (2016) there is a substantial positive link between profits management via DAs or REM and EVA. Furthermore, REM activities have a stronger explanatory power in these countries. Furthermore, Wang, Jiang, Liu, and Wang (2015): Earnings Management via Discretionary Accruals (Jones model, discretionary working capital accruals) is positively related to uncorrected EVA, but negatively related to adjusted EVA (join adjusted elements). Further research revealed that Earnings Management through DAs (current DAs) has a significant negative correlation to adjusted EVA (combined adjustments plus economic depreciation adjusted items), and Earnings Management through DAs (Jones model, discretionary working capital accruals) has a significant positive correlation.

From the foregoing, it can be concluded that the economic value index is one of the important measures, but it needs to be developed and take into account other influences and studies that criticized this indicator.

Conclusion

From what has been presented in this paper. It is clear how important is the measure of Economic Value-Added? and preference that this measure has over traditional performance measures. This measure is based on creating value for the company, and this measure is distinguished by taking into account invested capital, whether owned or borrowed. In addition, studies have shown that the measure of Economic Value Added? increases the performance of the company and the performance of the management working. This measure affects the market value of the company and its use leads to maximizing the wealth of shareholders, and like all performance measures he has supporters and has critics. One of the criticisms directed against him is that he measures performance on the short level, as he cares about results, not causes, and the most important criticism directed at him is his dependence on accounting profit in the financial statements whether these statements represent the actual performance of the company or not.

References

[1] Amarvathi, M and Raja, S. (2014). Optimum capital structure strategy and Usage of Economic Value Added? for shareholders Value creation with special reference to Infosys, India Journal of Applied Research, 4(12), 556-558 [2] Biddle, G. C., Bowen, M. R. & Wallace, J.S. (1999). Evidence on EVA. Journal of Applied Corporate Finance, 12(2), 69-79. [3] Biddle, G. C., Bowen, M. R. & Wallace, J.S. (1999). Evidence on EVA. Journal of Applied Corporate Finance, 12(2), 69-79. [4] Buhari, H. (2012). Value Based Performance Measures from a Shareholders Perspective: Between Theory and Application, Journal of the performance of Algerian institution, Issu 1. [5] Chen, L., & Qiao, Z. (2008). Improvement of EVA on Traditional Performance Measurement: An Application of Neural Network. 2008 Fourth International Conference on Natural Computation. doi:10.1109/icnc.2008.52 [6] Chen, S. & Dodd, J. L. (1997). Usefulness of accounting earnings, residual income, and EVA: A value-relevance perspective”, Unpublished Working paper, Clarion University. [7] Chen, S. and J. L. Dodd (2001), ‘Operating Income, Residual Income and EVA™: Which Metric is More Value Relevant?’, Journal of Managerial Issues, 13(1), pp. 65-86. https://www.jstor.org/stable/40604334. [8] Ehrbar, A. (1998), Economic Value Added?: The Real Key to Creating Wealth, New York: John Wiley & Sons, Inc. [9] Elmadhoun, I. R., & Reddy, G. N.(2022). The Effect of Real Earnings Management on Economic Value Added: Listed Companies of Dubai Financial Market. International Journal for Research in Applied Science & Engineering Technology (IJRASET), 10(1) 1577-1587. 10.22214/ijraset.2022.40071. [10] Erasmus, P. (2008). The relative and incremental information content of the value-based financial performance measure Cash Value Added (CVA). Management Dynamics: Journal of the Southern African Institute for Management Scientists, 17(1), 2-15. [11] Ferguson, R., Rentzler, J. & Yu, S. (2005). Does Economic Value Added? (EVA) improve stock performance or profitability? Journal of Applied Finance, 15(2). https://ssrn.com/abstract=2335465 [12] Grant, J. (2003), Foundations of Economic Value Added?, Second Ed., New York: John Wiley & Sons. [13] ? ?? ?Kim, G.W. (2006). EVA and Traditional Accounting Measures: which Metric is a better predictor of market value of hospitality companies? Journal of Hospitality & Tourism Research, 30(1), 34-49. https://doi.org/10.1177/1096348005284268 [14] ??Irala, L.(2007), Corporate performance measures in India: An Empirical Analysis. Social Science Research Network Electronic Journal. http://dx.doi.org/10.2139/ssrn.964375. [15] Jiambalov, J. (2007). Managerial Accounting 3th Edition, Jhon Wiley and sons Inc., New Yourk. [16] Lefkowitz, S.D. (1999). The Correlation between EVA and MVA of companies. MBA Dissertation, California State University. [17] Liu, Z. J. (2016). Effect of Earnings Management on Economic Value Added: A cross-country study. South African Journal of Business Management, 47(1), 29-36. https://doi.org/10.5430/afr.v4n3p9. [18] Liu, Z. J., & Wang, Y. S. (2017). Effect of Earnings Management on economic value ?added: G20 and ?African countries study. South African Journal of Economic ?and Management Sciences, 20(1), 1-9.? http://dx.doi.org/10.4102/sajems.v20i1.1247. ? ? [19] Lovata, L. M. and M. L. Costigan (2002). Empirical Analysis of Adopters of Economic Value Added?. Management Accounting Research, 13(2), pp. 215-228. https://doi.org/10.1006/mare.2002.0181 [20] O’Byrne, S. F. (1996). EVA and Market Value. Journal of Applied Corporate Finance, 9(1), pp. 116-125. https://doi.org/10.1111/j.1745-6622.1996.tb00109.x. [21] Peterson, P. P. & Peterson, D.R. (1996). Company Performance and Measures of Value Added. The Research Foundation of the Institute of Chartered Financial Analysts, Charlottesville, VA. [22] Ramana, D. V. (2005). Market value added and Economic Value Added?: Some empirical evidences. In 8th Capital Markets Conference, Indian Institute of Capital Markets Paper. http://dx.doi.org/10.2139/ssrn.87140? [23] Scott, M. (2001). Economic Value-Added? Joining Forces. Financial Management April, p36-37 [24] Sheehan, T. (1994), ‘To EVA or not to EVA: Is that a Question?’, Journal of Applied Corporate Finance, 7(2), pp. 85-87. [25] Siwasi, H. (2010). Study and analysis of indicators for measuring the performance of institutions from the perspective of value creation, Research Magazine Issu (7), Eygept. [26] Stern, J. M., G. B. Stewart III and D. H. Chew, Jr. (1995), ‘The EVA Financial System’, Journal of Applied Corporate Finance, 8(2), pp. 32-46. [27] Stewart, G. B. (1991). The Quest for Value: A Guide for Senior Managers, First Ed., New York: Harper Business. [28] Stewart, G. B. (1994). EVATM: Fact and Fantasy. Journal of Applied Corporate Finance, 7(2), pp. 71-84. [29] Stewart, G. B. (1999), The Quest for Value, Second Ed., New York: Harper Business. [30] Tully, S. (1993), ‘The Real Key to Creating Wealth’, Fortune, 128(6), pp. 38-50. [31] Turvey, C. G., L. Lake, E. Van Duren and D. Sparing (2000), ‘The Relationship between Economic Value Added? and the Stock Market Performance of Agribusiness Firms’, Agribusiness, 16(4), pp. 399-416. https://doi.org/10.1002/agr.10049. [32] Walbert, L. (1994). The Stern Stewart performance 1000: using Eva™ to build market value. Journal of Applied Corporate Finance, 6(4), 109-112. https://doi.org/10.1111/j.1745-6622.1994.tb00256.x. [33] Wang, Y., Jiang, X., Liu, Z., & Wang, W. (2015). Effect of Earnings Management on ?economic value ?added: A China study. Accounting and Finance Research, 4(3), ??9.? ? https://doi.org/10.5430/afr.v4n3p9.

Copyright

Copyright © 2022 Dr. Ibrahim R. I. Elmadhoun, Mohammed H. K. Murtaja. This is an open access article distributed under the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original work is properly cited.

Download Paper

Paper Id : IJRASET40450

Publish Date : 2022-02-21

ISSN : 2321-9653

Publisher Name : IJRASET

DOI Link : Click Here

Submit Paper Online

Submit Paper Online