Ijraset Journal For Research in Applied Science and Engineering Technology

A Study on Investment Pattern of General Public

Authors: Ms. B. M. Saranya, Dr. S. Joyce

DOI Link: https://doi.org/10.22214/ijraset.2022.41388

Certificate: View Certificate

Abstract

Investment is the use of finances with the goal of generating extra income and increasing the value of the asset. The Indian economy is booming, and there are numerous investment opportunities. Understanding individual investor behaviour could be extremely useful in explaining stock market oddities, as well as assisting policymakers and researchers in responding to varying investor behaviour. The current study is part of a larger investigation of the elements that influence the general public\'s investment patterns. This paper examines how different classes of people invest. The study will go through the investment patterns of working women, households, rural people, and salaried employees, as well as the investment patterns of the general public (a diverse category of people).

Introduction

I. INTRODUCTION

Investment is the use of finances with the goal of generating extra revenue and increasing the value of the asset. One of the most important characteristics of an investment is that it requires a period of waiting for a reward. It requires committing resources that have been saved or laid aside for future use in order to reap future benefits. Investment is the process of allocating monetary resources to assets that are expected to yield a gain or positive return over a given period of time. You must invest in order to achieve your goals. At the heart of every investment decision is a risk-reward trade-off. Bank deposits, real estate, small savings, life insurance plans, bullions, commercial deposits, corporate security-bonds, mutual funds, and equity and preference shares are all examples of financial instruments.

Investors' behaviour and investing pattern are shown by the amount of money they invest out of their overall savings, the frequency with which they invest, the financial instruments in which they invest, and their risk aversion.

II. INDUSTRY PROFILE

Post-independence India's Planning Commission has worked to attain economic development goals by establishing a prosperous environment for its citizens. Since the implementation of the "New Economic Policy," the country has experienced faster growth and an improvement in people's well-being, as measured by GDP and per capita income growth (PCI). There was a substantial increase in per capita income throughout the same period since GDP rose faster than the population. In the decade 2003-08, India was one of the world's fastest growing economies, surpassed only by China, which was also enjoying rapid growth. Despite breaking a three-year streak of growth rates above 9% and causing major macro-variables to fall, India's momentum since 2003 and the structure of international commerce allowed it to sustain a modest growth rate of 5.12 percent even in 2008-09, the year of the sovereign debt crisis. As a result of the crisis, growth declined after 2008-09. The financial crisis of 2009 has far-reaching consequences for every sector of the economy. The PCI's growth rate has slowed significantly. It has been noted that a rise in GDP and PCI is accompanied with a rise in the savings and investment rate. This is not a surprise result because, in developing countries, growth theory suggests that improving the savings rate will result in quicker growth and improved per capita statistics. Furthermore, a general rise in PCI leaves people with more money to save and invest than before, and they are more ready to renounce current consumption in exchange for more future. Since then, gross domestic savings have continuously dropped, reaching 30.5 percent of GDP in 2013-14. (Indian Macroeconomic Survey, December 22nd, 2014) The household sector contributes the most to savings (more than 20 percent of GDP).

When paired with other Economic and Social Factors, a high rate of investment is a good indication for any economy, and it should herald prospects for rapid growth for India. It's important to analyse all of the following information together. It highlights a tendency in India, in which a country's savings and investment rates climb in tandem with its GDP and PCI. Rather than a causal relationship where one variable rises as a result of the other, a correlation is noticed if both variables rise at the same time. An increase in a country's investment rate leads to higher capital formation, which leads to quicker growth, and faster growth leads to better PCI, which means more disposable income to save and invest.

A. Different Investment Avenues

- Shares: Direct equity investing is one of the best investment options for long term purpose. It is about the equity shares of a company, which binds you in legal terms related to the company ownership.

- Mutual Funds: Mutual funds are traditional investment options with a high rate of return. For many Indians, it is a good investment opportunity. People should heed the advise of consultants, specialists, and even agents and distributors. Mutual funds follow a very conventional cycle.

- Gold and Silver: Investing in gold and silver is still a conventional financial strategy today. There has never been a drop in investors’ interest in gold and silver since ancient times. They view it as a long-term investment..

- Real Estate: Since India's population has grown, there has been a huge increase in the number of properties and lands available for people to reside on. As a result, it has become a brilliant investment concept during the last few decades. It includes land, flats, houses, structures, agricultural fields, and many other types of investments.

- Bank deposit/ Fixed Deposit: The more senior society uses and trusts the fixed deposit the most. Banks provide fixed deposits as a deposit option. The procedure is simple; all you have to do is deposit a certain amount for a certain duration of time. The bank or another financial institution might pay you a predetermined interest rate on that money. This type of investment serves as a source of working capital for banks.

- Insurance: Insurance is a technique of safeguarding against financial loss. It's a type of risk management that's used mostly to protect against the danger of a speculative or uncertain loss.

- Bonds: Companies and government entities, like individuals, require funding for infrastructure development and social activities, for which they issue bonds to the public markets. The bonds are subsequently purchased by interested investors to assist these entities in raising funds. Bonds, in other words, are fixed-income investment choices that cover an investor's debt to a corporate or governmental borrower.

B. Objective Of The Study

- To review the investment pattern of different class of people.

- To give major findings in investment pattern of different class of people.

- To analyses the difficulties faced during investing in different avenues.

C. Need For The Study

The Indian economy is growing significantly and has various investment options. Understanding the individual investor behavior could be of great help in order to explain the stock market anomalies, to help the policy makers and the researchers to respond to the varying behavior of an investor.

III. REVIEW OF LITERATURE

Ajinkya Kumawat and Alka Parkar (2020) noted how age, income, and education are the major elements that influence an individual's investment decision.

Abhinandan, Aiman Alasbahi, Ebrahim, (2019) concluded that the investment behaviour of one class of people is different from another class of people, it may be in the form of risk perception level, awareness of various investment. Bank deposits are one of the most popular investment options for consumers of all income levels.

V. Dineshkumar (2018) investigated the investment patterns of individual investors, their investment techniques, and their expectations from their investments. Disha. A. Popat (2018) investigated the financial knowledge and perceptions of rural and urban investors in relation to risk and return when making financial decisions in various investment channels. The study was based on primary data gathered from 100 rural and 100 urban investors in Gandhinagar via a questionnaire. The data show that rural investors prefer low-risk, moderate-return opportunities, whereas urban investors prefer high-risk, high-return opportunities.

Parimalakanthi & Kumar (2015) observed that education of investors was an important aspect for investors in the city of Coimbatore as they wanted to gather as much information from sources like their friends, peers and investment experts as they could before arriving at an investment decision. Most of the investors invested in savings accounts followed by tangible instruments like Gold & Silver. They suggested that for many investors the investments were last resort rather than having a plan beforehand and investing according to it which was the reason for investments not doing very well.

Sonali Patil (2014) studied preferred investment avenues among salaried people with reference to Pune City, India. A sample size of 40 investors has been taken from the Pune City, India. The result of finding showed 60% investors were aware about the investment avenues whereas 40% were unaware.

Dr. Aparna Samudra, Dr.M.A.Burghate (2012) identified the research results bring out the fact that the saving of the selected households of the middle class are good but they don't want to save for long term or build a financial.

As per the study conducted by Lutfi (2010) Investors? education and income positively correlated with the risk tolerance ability of the investors. The result of his study also revealed that investors? risk behaviour positively correlated with the type of investment they select. Risk seeking Investors prefer to invest most of their money in riskier assets, mainly stocks, and put the residual in other assets, such as bank accounts and real assets. In general, the risk seekers are those who are single, well educated, relatively wealthy, and small family investors.

IV. RESEARCH METHODOLOGY:

The current study is part of a larger investigation of the factors that influence the general public's investment patterns. This paper examines how different classes of people invest. Based on past research, these groups of persons have been identified.

A. Research Design

In the beginning the research stage is exploratory because the research statement was developed on the basis of various review of literature that was available on internet and journals. After framing the research statement, the research design becomes descriptive as it is now describes the characteristics of a part of population as a sample for overall investment preference.

B. Sources Of Data

For the research both primary and secondary data is collected. The primary data for the study is collected directly from target respondents through structured questionnaire. The secondary data is collected from journal, articles, internet, reports, and other publications.

V. DATA ANALYSIS

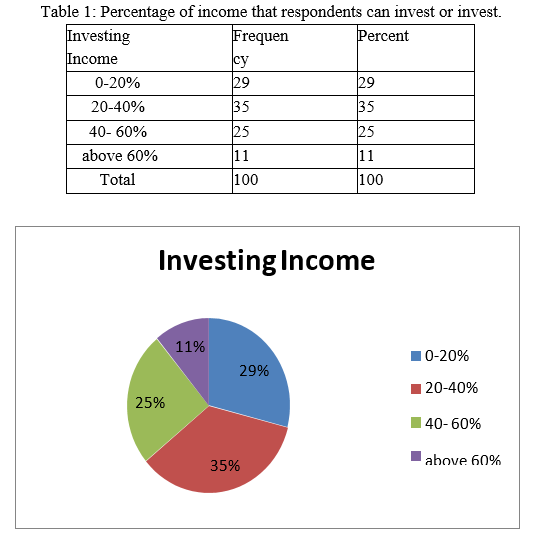

- Interpretation: From the above table it is interpreted that the number of respondents who prefer investing 0-20% is 29%, 20-40% is 35%, 40-60% is 25% and above 60% is 11%.

Majority (35%) of the respondents prefer to invest 20-40% of their income.

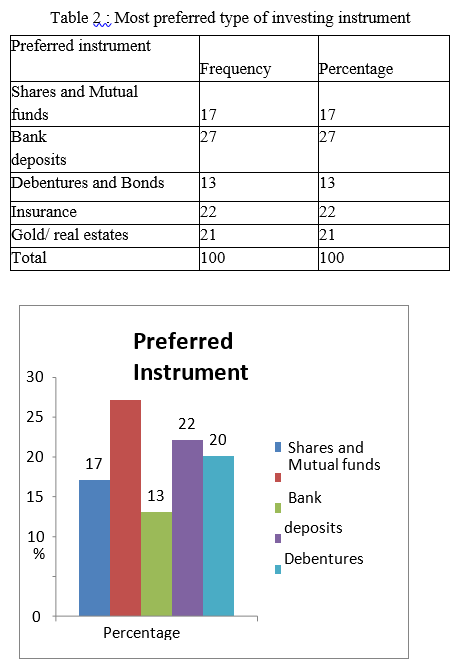

Table 2 : Most preferred type of investing instrument

- Interpretation: From the above table it is interpreted that the number of respondents who prefer Shares and mutual funds are 17%, bank deposit is 27%, debenture and bonds is 13%, insurance is 22% and gold real estates is 20%.

Majority (27%) prefer bank deposit as their preferred instrument.

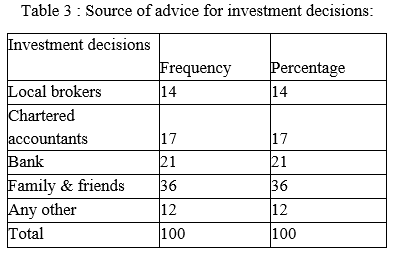

- Interpretation: From the above table it is interpreted that the number of respondents who seek advice related to investment decisions from Local brokers is 14%, Chartered accountants is 17%, Bank is 21%, Friends and family is 36% and Any other is 12%.

Majority (36%) of the respondents seek advice related to investment decisions from friends and family.

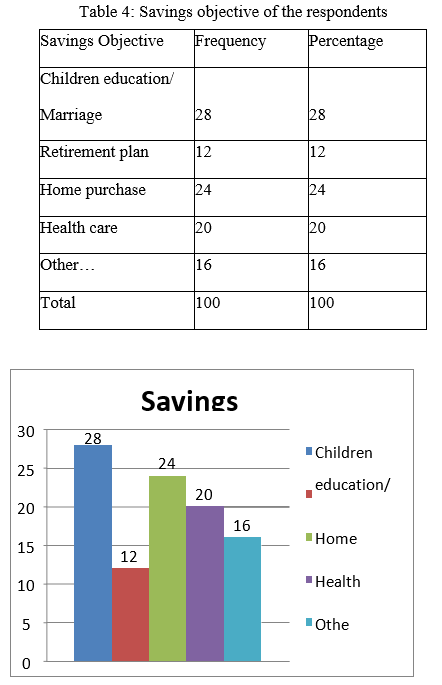

- Interpretation: From the above table, it shows the respondents savings objective choice. 28% of the respondents invest for children education/marriage, 12% invest for retirement plan, 24% invest in home purchase, 20% invest in health care and 16% invest in other objectives.

Majority (28%) of the respondents? savings objective choice is children education/marriage.

A. Hypothesis Testing

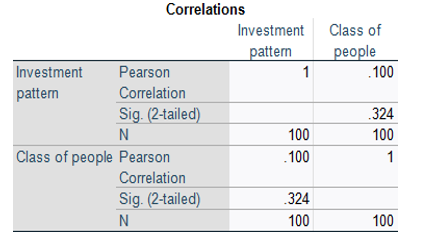

- Correlations

- Interpretation: Hence, Investment pattern and class of people are Positively Correlated.

2. Chi- Square Test

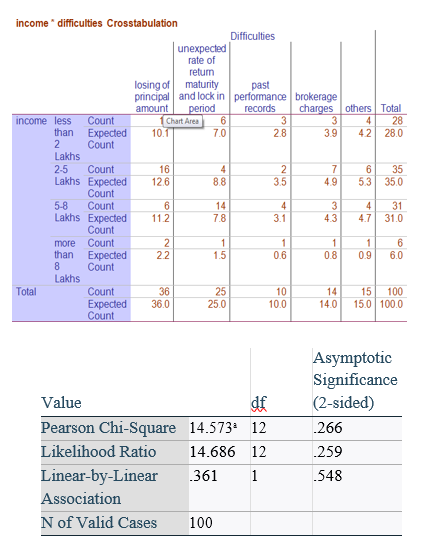

- H0 – Null hypothesis - there is no significant relationship between income and the difficulties faced during investing in different avenues.

- H1 – Alternative hypothesis - there is significant relationship between income and the difficulties faced during investing in different avenues.

13 cells (65.0%) have expected count less than 5. The minimum expected count is .60.

- Interpretation: Since 0.266 is greater than 0.05 at 5% level of significance, we should accept the Null hypothesis and reject the Alternate hypothesis. Hence, there is no significance difference between income and the difficulties faced during investing in different avenues.

V. SUGGESTIONS

According to the research, the majority of the population prefers bank deposits as their preferred investment strategy, indicating that they are only willing to invest in safe assets. Only 20-40% of their money is set aside for investment, with the majority of it going towards their children's education and marriage. The general people is more concerned about losing their money than about the instrument's risk and return. According to the study, the general population is unaware of various investment options and is concerned about investing challenges. As a result, the public can be given the following recommendations to help people understand investment and its possibilities.

A. Analyzing in detail about the instrument before investing.

B. Awareness regarding different avenues of investment

Conclusion

The research study uncovered a number of significant facts on respondents\' investment choices and investing challenges. When it comes to choices that are adhered before or during investment, descriptive study of demographic factors suggested that. The study\'s findings reveal that investment patterns and social class are favourably associated, with no significant difference between income and the obstacles faced when investing in various channels. This study can also be extended addressing all other factors for a wider scope and better understanding.

References

Articles; [1] N. Geetha, Dr. M. Ramesh, (2011), \'A Study on Peoples Preference in Investment Behaviour?, International Journal of Engineering and Management Research. Volume 1 Issue 6. [2] FCA Pratibha Chaurasia, (2017) \'A Study of Investment preference of investors, International Journal of Application or Innovation in Engineering and Management (IJAEIM). Volume 6 Issue 7. [3] U M Gopal Krishna, Aliya Sultana, T Naraya Reddy, (2019), \'Investors Perception towards Investment Avenues\', International Journal of Recent Technology and Engineering. Volume 8 Issue 2 quarterly bi-lingual research journal Vol. 7 Issue 25 January to March 2020 SHODH SARITA 243. [4] Dr. T. Sisil, S. Gokul Kumar, S. Sivakumar, G. Manikanda and V. Dineshkumar, (2018), \'A study on Investors behaviour on Investment Options\'. International Journal of Advance Research and Innovative Ideas in Education. Volume 4 Issue 3. [5] Dish. A. Popat, Dr. Hemal. B. Pandya. December, (2018), \'Evaluating the effect of Financial Knowledge on Investment decisions of Investors from Gandhinagar District\' . International Journal of Engineering and Management Research. Volume 8 Issue 6. [6] K.Parimalakanthi, Dr. M. Ashok Kumar, (2015), \'A Study Pertaining to Investment Behaviour of Individual Investors in Coimbatore City\', International Journal of Advance Research in Computer Science and Management studies. Volume 3 Issue 6. [7] Bharti Wadhwa, Aakanksha Uppal, Anubha Vashisht, Davinder Kaur, (2019), \'A Study on Behaviour and Preference of Individual Investors towards Investment with special reference to Delhi NCR\', International Journal of Innovative technology and exploring engineering (IJITEE). Volume 8 Issue 65. [8] Dr.P. Amaraveni, Mrs. M. Archana, (2017), \'A Study of Investors Behaviour towards various Investment Avenues in Warangal City\', Asia Pacific Journal of Research in Business Management. Volume 8 Issue 7.

Copyright

Copyright © 2022 Ms. B. M. Saranya, Dr. S. Joyce. This is an open access article distributed under the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original work is properly cited.

Download Paper

Paper Id : IJRASET41388

Publish Date : 2022-04-11

ISSN : 2321-9653

Publisher Name : IJRASET

DOI Link : Click Here

Submit Paper Online

Submit Paper Online