Ijraset Journal For Research in Applied Science and Engineering Technology

The Proactive Approach for Cost Control in Organizations

Authors: Mitali Saxena

DOI Link: https://doi.org/10.22214/ijraset.2022.40761

Certificate: View Certificate

Abstract

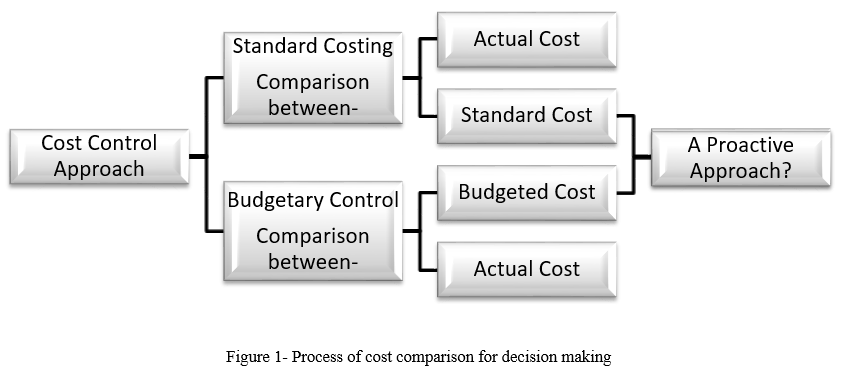

To run a company successfully, profit maximization is first and most important objective which can be simply achieved by cost minimization. In order to earn maximum profits, the cost of product should be minimized. We have two approaches with us to estimate and plan the upcoming costs i.e. Standard Costing and Budgetary Control. We calculate variances in standard costing by comparing standard costs with the actuals which makes it a reactive approach. On the other hand we prepare budgets (estimations) which are regularly monitored and compared with the actuals so that corrective action can be taken if required. This again makes the process reactive. In this research paper we will see whether mixing of these two approaches results into a proactive approach which will help companies make a decision before committing a mistake.

Introduction

I. INTRODUCTION

CIMA defines standard cost as “A standard expressed in money. It is built up from an assessment of the value of cost elements. Its main uses are providing basis for performance measurement, control by exception reporting, valuing stock and establishing selling prices.” It is a pre-determined cost based on the previous trends. Budgeted (estimated) cost is an approximate assessment of what the cost will be. It is based on the anticipated future changes.

In standard costing we get variances after calculating the difference between standard cost and actual cost, whereas in budgetary control we calculate the difference between budgeted cost and actual cost to get the final results. Inclusion of actual cost in both the methods makes them a reactive approach. Which means decision is taken after the mistake has taken place. If we eliminate actual costs from both these methods and start calculating the difference between standard cost and budgeted cost, will this result in a proactive approach? If yes, then decisions regarding costs can be taken before committing a mistake.

II. OBJECTIVE AND METHODOLOGY

The main objective of this research is to find out a proactive approach that may help managers in controlling the cost before incurring them. The methodology used is completely experimental.

III. RESULTS AND DISCUSSION

Let us discuss with the help of an example, how comparison of standard cost and budgeted cost can help managers in making proactive decisions.

|

Fredrick Path labs Ltd. (Amount in Rs.) |

|||

|

Costs |

Standards |

Budgets |

Difference Favourable (F) Adverse (A) |

|

10,000 units |

10,000 units |

||

|

Variable costs |

|||

|

Raw Materials |

50,000 |

60,000 |

10,000 (A) |

|

Direct Labour |

84,000 |

76,000 |

8,000 (F) |

|

Overheads |

37,000 |

37,300 |

300 (A) |

|

Fixed Costs |

|||

|

Rent |

9,000 |

9,000 |

- |

|

Depreciation |

6,000 |

6,000 |

- |

|

Total |

1,86,000 |

1,88,300 |

2,300 (A) |

Table 1*

*In the above table, standard costs as per previous trends and budgeted costs after future assessment are given for the production of 10,000 units.

From the above table we can see that the company can suffer an overall cost of Rs. 2,300 in future. This adversity can be seen in forthcoming period because of the following reasons-

- There is an adverse amount of Rs. 10,000 in raw materials which is needed to be reduced in order to control the cost. It will be the responsibility of purchase manager to make quick decision in order to avoid this adversity in actual. Since the production manager is aware about the future cost increment, he can avoid the same to the possible extent and save the company’s cost.

- In case of direct labour, the company is having favourable difference and hence no further decision making will be required which will save the time of factory manager and the same time can be made effective by investing it in some required areas.

- In case of the variable overheads, there is an adverse amount of Rs.300 which is immaterial for the company and hence can be ignored.

- There is no difference in fixed costs and hence can be ignored.

Since we made a comparison between standards and budgets, the managers can make required decisions on time before actually incurring the costs resulting into a proactive approach, which on the other hand would have been a reactive approach if we inserted actual costs into it.

Conclusion

When we follow standard costing, we find out variance and then we realize what changes are required in further process of production. Similarly, when we use budgetary control, we realize that we did not stand with the targets after actually incurring the cost. Both methods help in cost decision making but ultimately both are reactive methods. Instead of considering the actual figures with budgets and standards, if companies compare standards with the budgets, they can realize in advance what good or adverse will happen in future after actually incurring the costs. If this proactive approach is used, decisions can be taken at early stage and managers can save time as well as control costs as per the requirements

References

[1] www.transtutors.com [2] Principles of Accounting. Vol. 2. Managerial Accounting from www.opentextbc.com [3] My Accounting Course. Budgeted Cost from www.myaccountingcourse.com [4] Sankalp Kanstiya, Shreya Kanstiya, (2019). Strategic Cost Management and Performance Evaluation Optimised 4.0. Vol. 1. No. 10 & 11

Copyright

Copyright © 2022 Mitali Saxena. This is an open access article distributed under the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original work is properly cited.

Download Paper

Paper Id : IJRASET40761

Publish Date : 2022-03-12

ISSN : 2321-9653

Publisher Name : IJRASET

DOI Link : Click Here

Submit Paper Online

Submit Paper Online