Ijraset Journal For Research in Applied Science and Engineering Technology

Stock Time Series Prediction Using Machine Learning Techniques

Authors: Ganti Rohini Krishna Sindhu, Lakshmi Prasanna Penumatsa, Amrutha Varshini Mavuri, Rishitha Alla, Dr. Dwiti Krishna Bebarta

DOI Link: https://doi.org/10.22214/ijraset.2023.50643

Certificate: View Certificate

Abstract

Stock is a place where buying and selling of shares be for intimately listed companies and stock exchange is the middleman that allows buying and selling of shares. Stock request vaticination is a grueling task due to the largely noisy, complex and chaotic nature of the stock price data. The intraday patterns are linked using the point engineering schemes and several machine literacy techniques. The deep literacy styles are combined with rearmost machine literacy models to rognosticate the direction of the ending price. Accuracy plays an important part in stock request vaticination. Although numerous algorithms are available for this purpose, opting the most accurate one continues to be the abecedarian task in getting the stylish results. In order to achieve this we\'re combining different models and creating a hybrid model( LSTM with GRU) which provides better accuracy.

Introduction

I. INTRODUCTION

A. Objective

The charm of getting profit by suitably investing the stocks in the stock market attracts thousands of investors. Since every investor wants profit with lower threat, they need realistic models to prognosticate the stock price. As investors are investing further and further plutocrat in the market, they get anxious to know the unborn trends of the colorful stocks available in the market. The major part of the trends in the market is to know when to buy, hold or vend the stocks. Stock market vaticination is observed as a grueling task because of high change and irregularity. therefore, multitudinous models have been depicted to give the investors with more precise prognostications. Stock market has attracted a lot of exploration interests in former literature. With a successful model for stock vaticination, we can gain insight about market behavior over time, spotting trends that would else not have been noticed. With the increasingly computational power of the computer, machine learning will be an effective system to solve this problem. still, the public stock dataset is too limited for numerous machine learning algorithms to work with. We want to introduce a framework in which we integrate user predictions into the current machine learning algorithm using public historical data to improve our results. The motivated idea is that, if we know all information about moment's stock trading( of all specific dealers), the price is predictable. therefore, if we can gain just a partial information, we can expect to improve the current prediction a lot. With the growth of the Internet, social networks, and online social relations, getting daily user predictions is a doable job. therefore, our motivation is to design a hybrid model or a stronger model that will profit everyone.

B. Problem Definition

The rate of investment and business openings and benefit of the investors in the Stock market can increase if an effective algorithm could be used to predict the short term closing price of an individual stock. The predicted results can be used to help the former styles of stock predictions which has an error loss at an normal of 20. The overall ideal of my work will be to predict accurately the ending price of the stock. Attributes considered form the primary base for tests and give accurate results more or less. multitudinous farther input attributes can be taken but our thing is to predict with numerous attributes and faster effectiveness the ending price of stock. opinions are constantly made predicated on the knowledge rich data hidden in the data set and databases. We want to produce a model that has stronger capability to predict the ending price of stock..

C. Background

There are existing methodologies which are proposed in the field of stock time series data prediction system. There are existing works using machine learning techniques to provide a solution to the problem. But there are certain drawbacks like limited extent to which data is used, the accuracy is quite unsatisfactory and there is a scope for improvement. Thus, to provide a solution using machine learning techniques is to ensure these problems are taken care of.

In this project, a solution to the problem of the stock time series data prediction system has been proposed. It is done mainly using machine learning techniques but in a more innovative manner, here. The Hybrid model can predict better results.

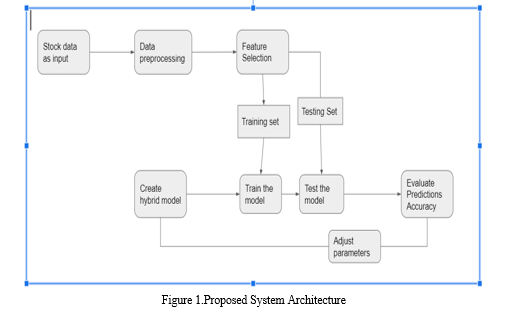

II. Proposed system

After evaluating the results from the existing methodologies, we are not able to predict the price of time series stock data for the data obtained from the datasets. Inorder to achieve this, we are using various algorithms such as Decision trees, linear regression, Support vector machine (SVM) and KNN with hybrid models. ML process starts from a preprocessing data phase followed by feature selection based on data cleaning, classification of modeling performance evaluation. Hybrid Decision trees using KNN Model technique are used. We are comparing the various performance parameters of the algorithms and finally choosing the best one to improve the accuracy of the result. We are using the KNN model to predict the future closing price of the stocks in time series pattern. Our study is based on two major parts : The pre-processing phase, when we choose the relevant attributes, and the second one applies a machine learning algorithm in order to select the algorithm that gives better accuracy. Hybrid decision trees and linear regression using KNN Model is the proposed approach used to improve the accuracy of the result. Our proposed system is divided into several phases.

A. Proposed System Architecture

III. PREDICTION MODELS

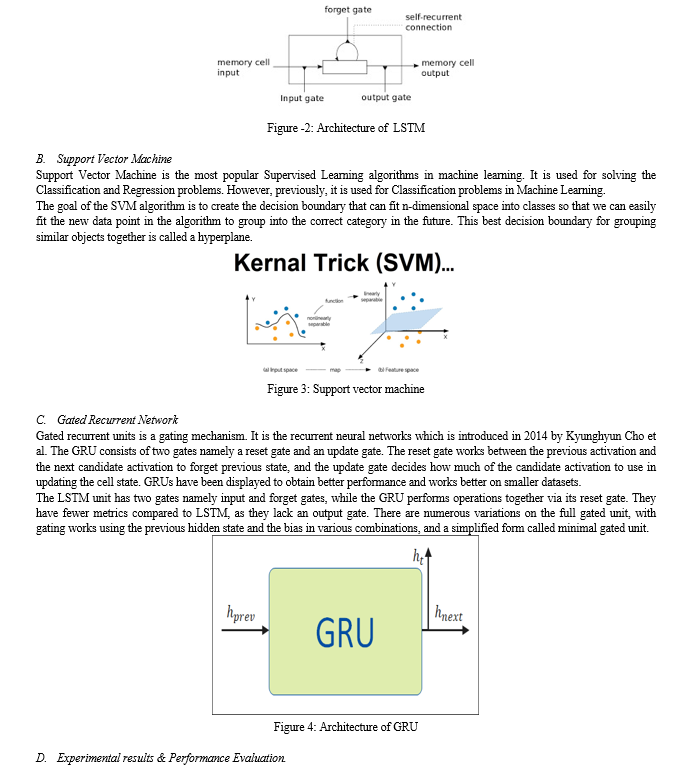

A. Long short time memory

Long short- term memory units are a structure unit for layers of a recurrent neural network( RNN). The Long Short- Term memory is a recurrent neural network is trained using Backpropagation through time and overcomes to break the grade problem. A LSTM unit is consists of three gates such as a cell, an input gate and a forget gate. The cell takes and remembers the values over time intervals from given data. thus it works like a memory in LSTM to store formerly information and use it for farther prediction. Each of the three gates can be allowed as a conventional artificial neuron, as in a multi- subcaste neural network that is, they calculate an activation of a weighted sum. still, they can be allowed as regulators of the block of values that goes through the connections of the LSTM. thus it obtains the output value from the output gate producing outputs as 0 or 1. still, also the information is not needed for the prediction, If the output produced is 0. still, also the information is suitable for the farther prediction of target value, If the output attained is 1. These connections between the gates and the cell made possible to predict the outputs.

Conclusion

The project titled Stock market time series data prediction using machine learning techniques is implemented using the machine learning models namely LSTM and GRU which are modern versions of Recurrent neural networks. The LSTM and GRU models are trained by feeding past datasets and statistics upon which it has learned and adapted to the pattern and predicted the future stock price value, which is approximate and close to the original value.

References

[1] Hua-Ning Hao, “Short-term Forecasting of Stock Price Based on Genetic-Neural Network”, 2010 Sixth International Conference on Natural Computation (ICNC 2010), IEEE Conference Publications. [2] Chen, W, Zhang, Y, Yeo, C.K., Lau, C.T., Lee, B.S. Stock market prediction using neural networks through news on online social networks[C]. Smart Cities Conference (ISC2), 2017 International, 2017: 11-2. [3] S. Selvin, R. Vinayakumar, E. A. Gopalakrishnan, V. K. Menon and K. P. Soman, \"Stock price prediction using LSTM, RNN and CNN-sliding window model,\" 2017 International Conference on Advances in Computing, Communications and Informatics (ICACCI), Udupi, 2017, pp. 1643-1647. [4] M. Q. Nelson, A. C. M. Pereira and R. A. de Oliveira, \"Stock market\'s price movement prediction with LSTM neural networks,\" 2017 International Joint Conference on Neural Networks (IJCNN), Anchorage, AK, 2017, pp. 1419-1426. [5] K. Chen, Y. Zhou and F. Dai, \"A LSTM-based method for stock returns prediction: A case study of China stock market,\" 2015 IEEE International Conference on Big Data (Big Data), Santa Clara, CA, 2015, pp. 2823-2824. [6] A. J. P. Samarawickrama and T. G. I. Fernando, \"A recurrent neural network approach in predicting daily stock prices and application to the Sri Lankan stock market,\" 2017 IEEE International Conference on Industrial and Information Systems (ICIIS), Peradeniya, 2017, pp. 1-6. [7] A. S. Chen, M. T. Leung, and H. Daouk, “Application of Neural Networks to an emerging financial market: Forecasting and trading the Taiwan Stock Index”, Comput. Operations Res., Vol-30, pp. 901-923, 2003.

Copyright

Copyright © 2023 Ganti Rohini Krishna Sindhu, Lakshmi Prasanna Penumatsa, Amrutha Varshini Mavuri, Rishitha Alla, Dr. Dwiti Krishna Bebarta. This is an open access article distributed under the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original work is properly cited.

Download Paper

Paper Id : IJRASET50643

Publish Date : 2023-04-19

ISSN : 2321-9653

Publisher Name : IJRASET

DOI Link : Click Here

Submit Paper Online

Submit Paper Online