Ijraset Journal For Research in Applied Science and Engineering Technology

Time-Series Forecasting: Predicting Stock Index Using Arima and Facebooks Prophet Model

Authors: Sushma Niveni Pindiga, DInesh Motati, Nikhil Gurram

DOI Link: https://doi.org/10.22214/ijraset.2022.45073

Certificate: View Certificate

Abstract

The DJIA is a New York Stock Exchange volatility index that incorporates the 30 maximum widespread shares inside the U.S stock market. Since the stock market is based totally on threats and speculations, forecasting the DJIA index helps us know the trends of 30 companies indexed. As a result, it helps investors of these 30 companies to be cautious. But forecasting these stock indexes could be challenging to assess as they were affected by various causes, making the prediction inaccurate. Throughout the paper, specific modifications had been accomplished at the version to increase the optimum variables to result in a minimal range of errors. This Project calls for thorough studies of the volatility of the economic marketplace and the various factors that affect it. Hence, this Project will serve economic analysts and investors to observe their analysis or investment selections by lowering the uncertainty.

Introduction

I. INTRODUCTION

The process of analysing and managing the time series data is known as Time series analysis. Time series analysis, in contrast to regression analysis, is constructive in finding essential features of time series data. Time series analysis help us understand the major factors that lead to a specific trend in time series data points and help us to predict data points. It is only a hopeful dream to be able to see into the future. Nonetheless, a driving factor for statisticians and theorists is their attempts to develop new models and methods to achieve as accurate forecasts as possible. One way to do this is by studying a company and the market where the company is established by work on fundamental analysis. However, technical analysis is the most crucial element in forecasting and is based on historical data on the price of a stock. These price movements are fundamental drivers for the next day, month or year predicted price. Models can be extended to get more predictable forecasts by adding more dividends, technical improvement, or a crisis. Knowing when to quit is the true problem since failing to do so might result in poor performance, erroneous findings, and a time-consuming process, which brings us to the paper's main question. Which model has the better forecasting ability when predicting the value of the Dow Jones Industrial Average Index? We want to investigate how our models will react to this. We will investigate this when we evaluate a model's performance when predicting the Dow Jones Industrial Average price. It is well known that the stock market is built on the expectation that is influenced by dividends, technology progress, innovations, and other announcements. Stock-price may also rely on other parameters such as vacations, holidays, or even weather. These parameters can be used to test a hypothesis or find a trend, notified as a cyclical pattern in the time-series data.

This paper will use the one-time price Dow Jones Industrial Average to forecast future price movements. We are going to apply two different models. The Autoregressive Integrated Moving Average Model (ARIMA) will be the first model we utilize, and the Facebook Prophet model will be the second model. The autoregressive integrated moving average, also known as ARIMA, is an analytical analysis model. It uses predicted time series data for further analysing the data set or to forecast future trends. Based on the past value, the analytical analysis model predicts the future values. Furthermore, the ARIMA model can predict the stock's future price using past perforation. It can predict the future possibility of the share price. ARIMA model introduces an order of differencing into the time-series data if the data is non-stationary. Dickey-Fuller test is used to verify data stationarity.

- AR (p) Auto-regression: the relationship between a current series and observation over a previous step. (p) Point out the use of preceding values in the regression equalization for foretelling the current one.

- When performing the time series stationary, I (d) Integrated employs the difference of observations, which includes subtracting the current values from their prior values (d) number of times.

- MA (q): A moving average component shows the inaccuracy of the model as a combination of prior mistakes. The number of words that will be added to this model is indicated by the sequence (q).

Facebook Prophet is a tool designed to let you easily predict time series at a large scale. The three main components of Facebook Prophet's analysable time series model are Trends, Holidays, and Seasonal. The combination of effect and error are mentioned below:

Before deciding to use Facebook prophet, some data characteristics should be met:

- Every hour, every day, or weekly research within a few months (at least one month), but one year of old data is much favoured.

- Holding powerful seasonality’s: day of the week and time of the year

- Significant events or festivals that happen must be seen.

- A moderate amount of missing or outlier data

- Past trend trades

We will finally evaluate and compare which models create the most accurate forecasts when predicting Index Values.

II. LITERATURE REVIEW

The authors [N Viswam] and [G Satyanarayana Reddy] [ 1] tried to implement a model which forecasts the share market trends by taking the company's previous historical time series data. They used the ARIMA model to make predictions to help investors to decide whether they can buy a stock or they can sell it. This implementation was done through R language and the drawback is that they can try to implement in python and compare the results with that of the R language for better accuracy.

Forecasting the stock exchange is one of the significant financial subjects. The authors Mahantesh C. Angadi, Amogh P. Kulkarni developed an Arima model and forecasted the stock market trends for a short period using previous historical data and data mining techniques. The results indicated that the model be applied for short-term forecasting.

In this work, the authors [B. Uma Devi1], [D.Sundar] and [Dr. P. Alli] [2] developed an Arima model which predicted trends of Nifty Midcap-50. They followed the BoxJenkins method to identify the model and AICBIC test principles are applied opposite to the data presented in the previous to decide on the best model.

The authors [Tayman],[ Jeff, et al ] [7] implemented six different arima models indicating variety of population growth trajectories. They implemented six different models using the data from four different states in United States. Research on other methods to measure uncertainty is also needed

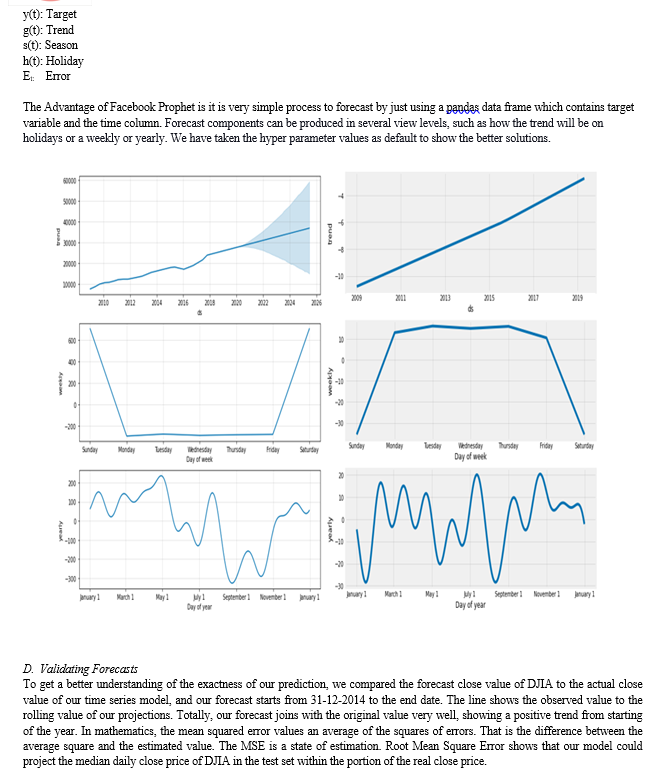

III. RESULTS AND DISCUSSION

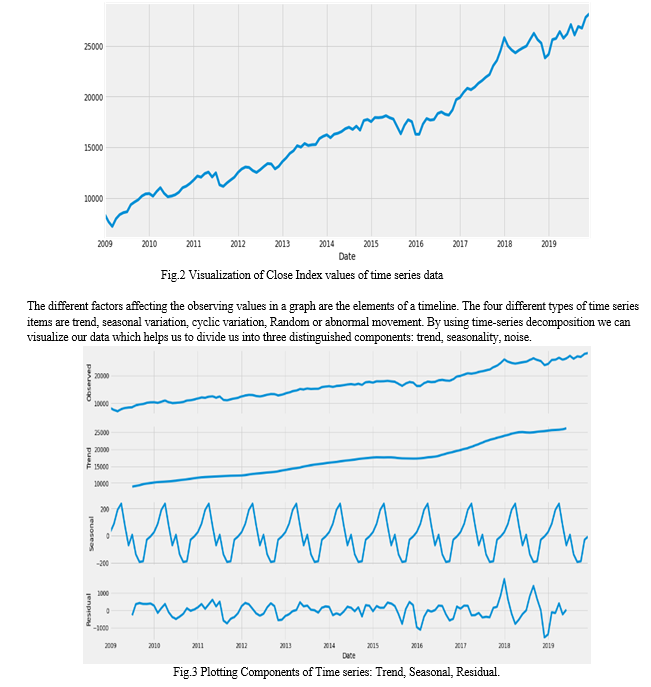

In this project, we collected data on Dow Jones Industrial Average from (2009-2019). We forecast the stock price using Time series forecasting with the ARIMA model and Facebook Prophet.

The complete architecture of the system is shown below.

A. Data Insights

We cannot comprehend the present or glance of our future if we cannot know our past which links to time-series forecast; we cannot decide which approach, we will use, we cannot predict future results accurately. This process includes getting the dates which has highest and lowest index values at a given time interval. Moreover, grouping the dates and visualizing the index values for each year to get a complete picture.

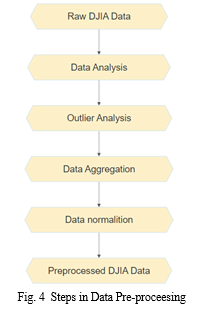

???????B. Data Pre-Processing

The Data Pre-processing involves applying of some data wrangling techniques on raw data to make it ready for model fitting. This includes removing unwanted columns, check missing values, aggregate index value of stocks by date. It includes some data cleaning tasks such as working with missing values and inconsistent data. This method also includes detection of outliers and fixing them.

???????C. Model Fitting

1) Approach 1: Using Autoregressive integrated moving average model

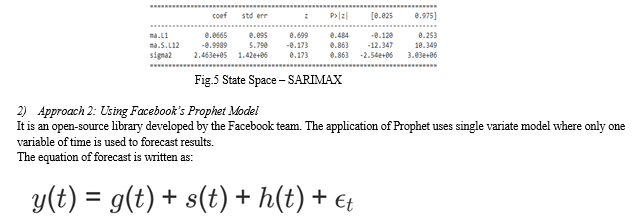

It uses predicted time series data of DJIA index for further analysing the data set or to forecast future trends which as a result forecasts the closing share value. ARIMA forecasts is more accurate and reliable. ARIMA is running easily with only one variable and cannot exploit leading indicators variables. The index value has been complicated and commonly related to a set of observable variables.

The SARIMAX class is an instance of a full-fledged model built applying the state space backend for evaluation. The output object has many attributes and techniques we could exact from other stats models outputs objects, involving standard errors, prediction/forecasting, and z-statistics.

Conclusion

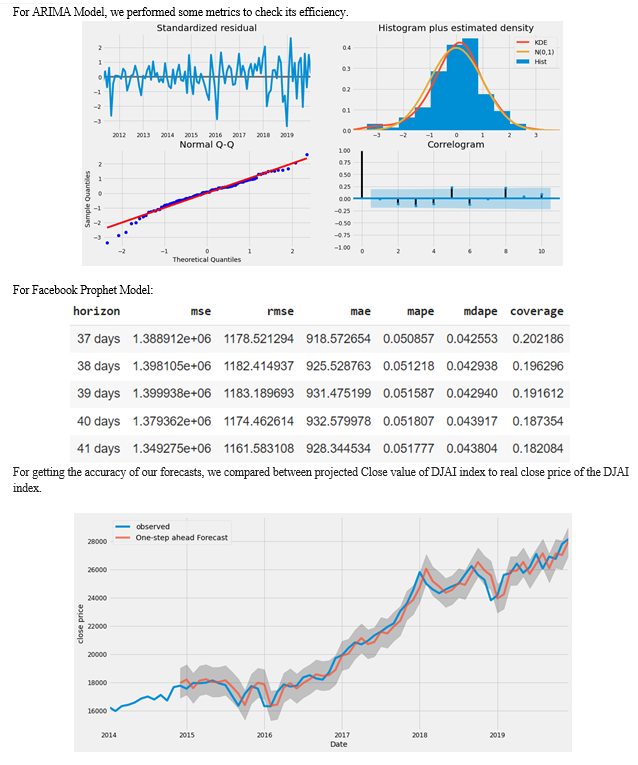

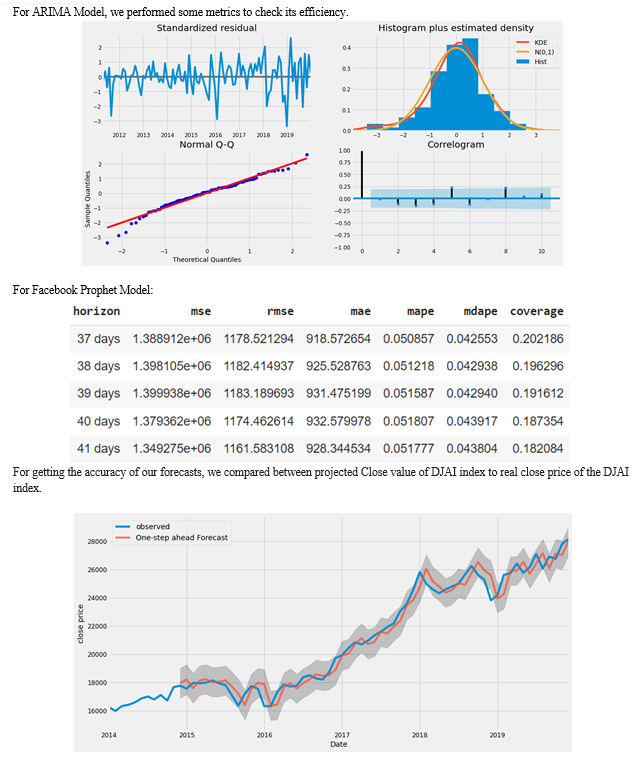

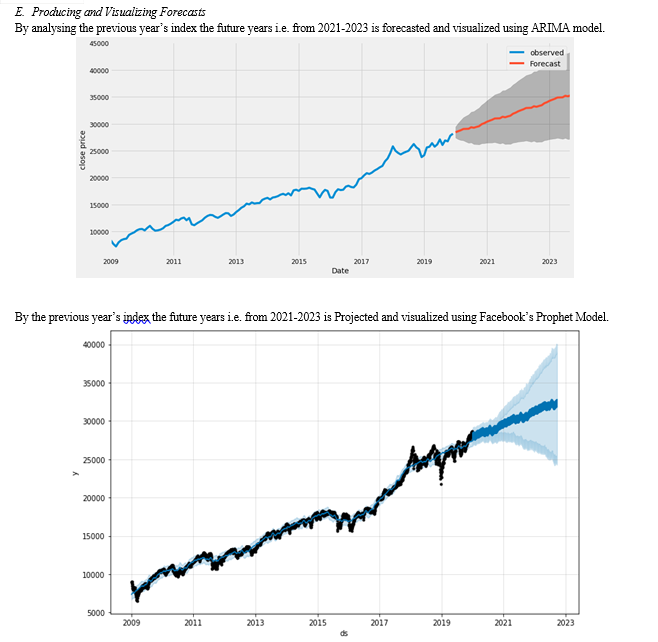

We tried to find out the best approach between ARIMA and Facebook prophet to forecast the DJIA index. ARIMA models play a very crucial role in predicting short-term momentum in the stock market. We calculated RMSE and MSE values to tell the reader which technique is better to forecast future prices. Our complete research suggests that forecasting using ARIMA gives minor errors than Facebook prophet. So we need to observe these predictions more carefully to get a favourable outcome because the stock market is crucial. We need to compare these time series models to help us identify the further possibilities of the Dow Jones Industrial Average Index.

References

[1]. N Viswam. Stock market prediction using time series analysis, International Journal of Statistics and Applied Mathematics 2018; 3(1): 465-469 [2]. B. U. Devi, D. Sundar, and P. Alli, “An Effective time series analysis for stock trend prediction using ARIMA model for Nifty Midcap-50,” International Journal of Data Mining & Knowledge Management Process, vol. 3, no. 1, pp. 65–78, 2013. [3]. P. Fen “An empirical study on the stock price analysis and prediction based on ARMA model,” Journal of Mathematics in Practice and Theory, vol. 41, no. 22, pp. 84–90, 2011. [4]. Jarrett E Jeffrey, ARIMA modeling with intervention to forecast and analyze Chinese stock prices, International Journal of Engineering Business Management, 2011; 3(3) [5]. Hanias “Prediction with Neural Networks: The Athens Stock Exchange Price Indicator”, European Journal of Economics, Finance and Administrative Sciences, Vol 9, pp. 21–27, 2007. [6]. Perez-Rodriguez, Forecasting Performance on the Spanish IBEX-35 Stock Index’, Journal of Empirical Finance, Vol 12, No 3, pp. 490–509, 2005. [7]. Tayman, Jeff, et al. \"Precision, Bias, and Uncertainty for State Population Forecasts: An Exploratory Analysis of Time Series Models.\" Population Research and Policy Review, vol. 26, no. 3, Springer, 2007, pp. 347-69 [8]. Wanyonyi Maurice, Dominic Makaa Kitavi, David Muchangi Mugo and Edwin Benson Atitwa, \"Covid-19 Prediction in Kenya using the Arima Model\", International Journal of Electrical Engineering and Technology (DJEET), 12(8), 2021, pp. I05-114.

Copyright

Copyright © 2022 Sushma Niveni Pindiga, DInesh Motati, Nikhil Gurram. This is an open access article distributed under the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original work is properly cited.

Download Paper

Paper Id : IJRASET45073

Publish Date : 2022-06-29

ISSN : 2321-9653

Publisher Name : IJRASET

DOI Link : Click Here

Submit Paper Online

Submit Paper Online